How Liquid Restaking and LRTs Work: A Non-Developer’s Map

How Liquid Restaking and LRTs Work: A Non-Developer’s Map (and Where I Drew It Wrong)

The first time I tried to draw how liquid restaking and LRTs work, I drew it wrong. I sketched a tidy ladder — stake ETH, earn a base yield, then stack a second yield on top, free money for doing nothing extra. That ladder is the version most explainers sell. It is also the version that quietly hides the one thing you actually need to see.

I am not a trader. I am a Korean office worker who reads crypto mechanics on weeknights to figure out what the structure means for someone like me, not what the price will do. So this is not a “best LRT to buy” piece. There is no buy here at all. It is the map I redrew after I noticed my first one was missing a layer — the layer where the same ETH ends up backing several promises at once.

Here is what you get: a plain definition, a layer-by-layer map from staking up to LRTs, the rehypothecation structure I missed on my first pass, an honest look at the risk stack, and where the word “liquid” stops being true.

The shortest honest definition

Liquid restaking is the practice of taking ETH that is already staked, restaking it to secure additional services beyond Ethereum itself, and receiving a tradeable token that represents that whole position. That token is an LRT — a liquid restaking token. You keep something you can move and use in DeFi while your underlying ETH does two jobs instead of one.

That is the textbook line. The interesting part is the word “additional.” Additional yield comes from additional work, and additional work means additional ways to lose. EigenLayer’s own documentation lays out the restaking concepts and the actors involved if you want the primary source. My job here is to translate it into a map a non-developer can hold in their head.

The map, one layer at a time

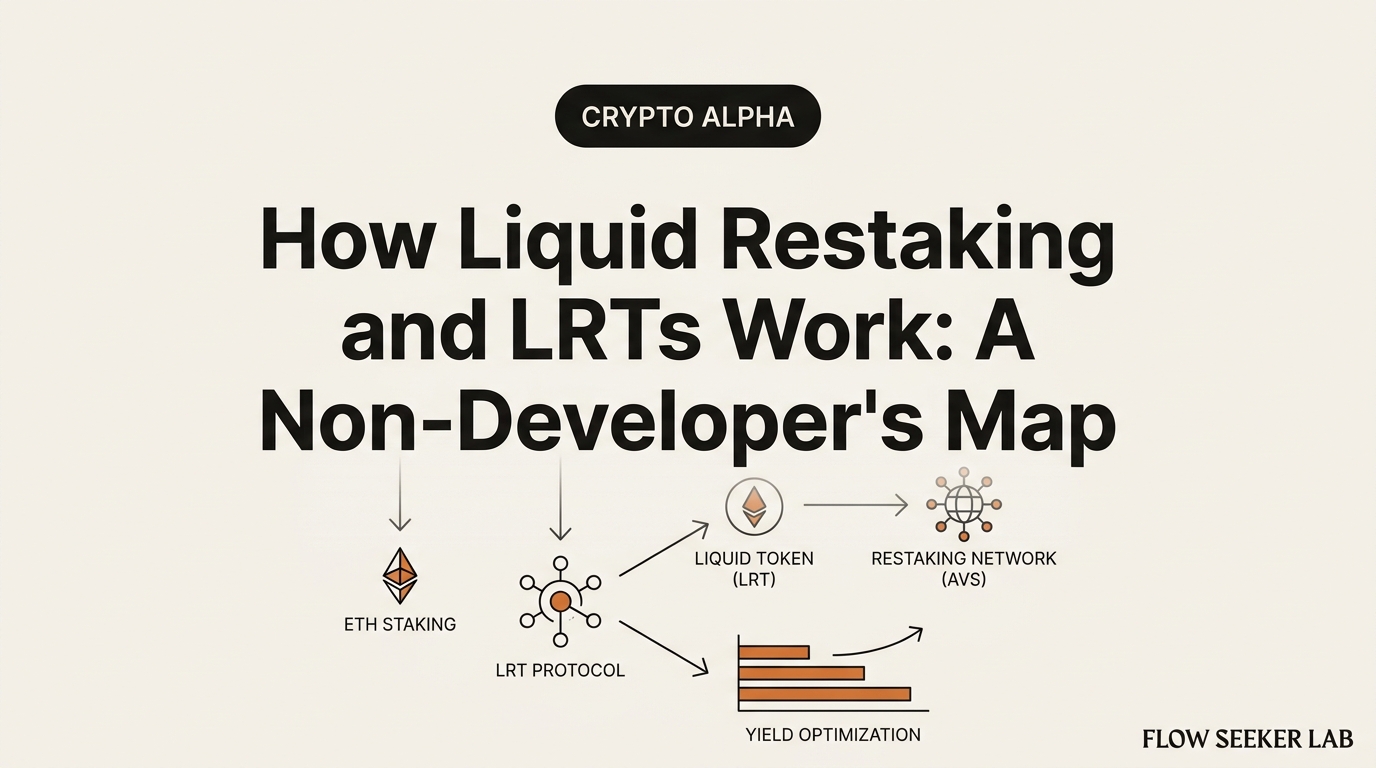

The cleanest way I found to understand this was to stop thinking “stake plus bonus” and start drawing layers, bottom to top. Each layer adds a job for your ETH, and each job adds a yield and a risk. Miss a layer and the whole thing looks like free money.

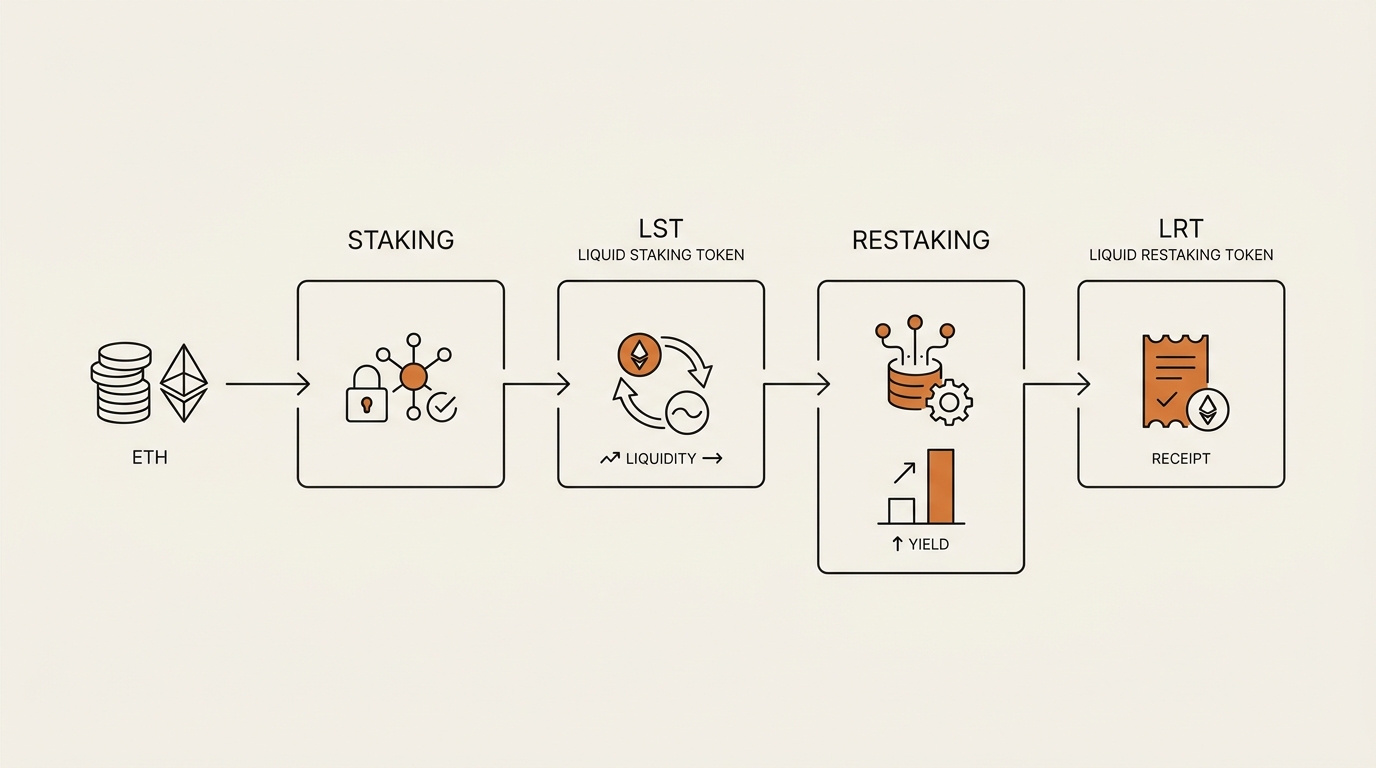

Layer 1 — Staking. You lock ETH to help validate the Ethereum network. In return you earn the base staking reward. This is the foundation Ethereum’s own guide to staking describes: your ETH secures the chain, and if your validator misbehaves, a slice of it can be removed. That removal is called slashing. Hold that word — it comes back at every layer above.

Layer 2 — Liquid staking. Locking ETH directly is illiquid; you cannot spend it while it validates. Liquid staking solves that. You deposit ETH with a protocol, it stakes on your behalf, and it hands you a liquid staking token, or LST, that you can move and trade. The LST represents your staked ETH plus its accruing reward. Lido’s stETH is the best-known example.

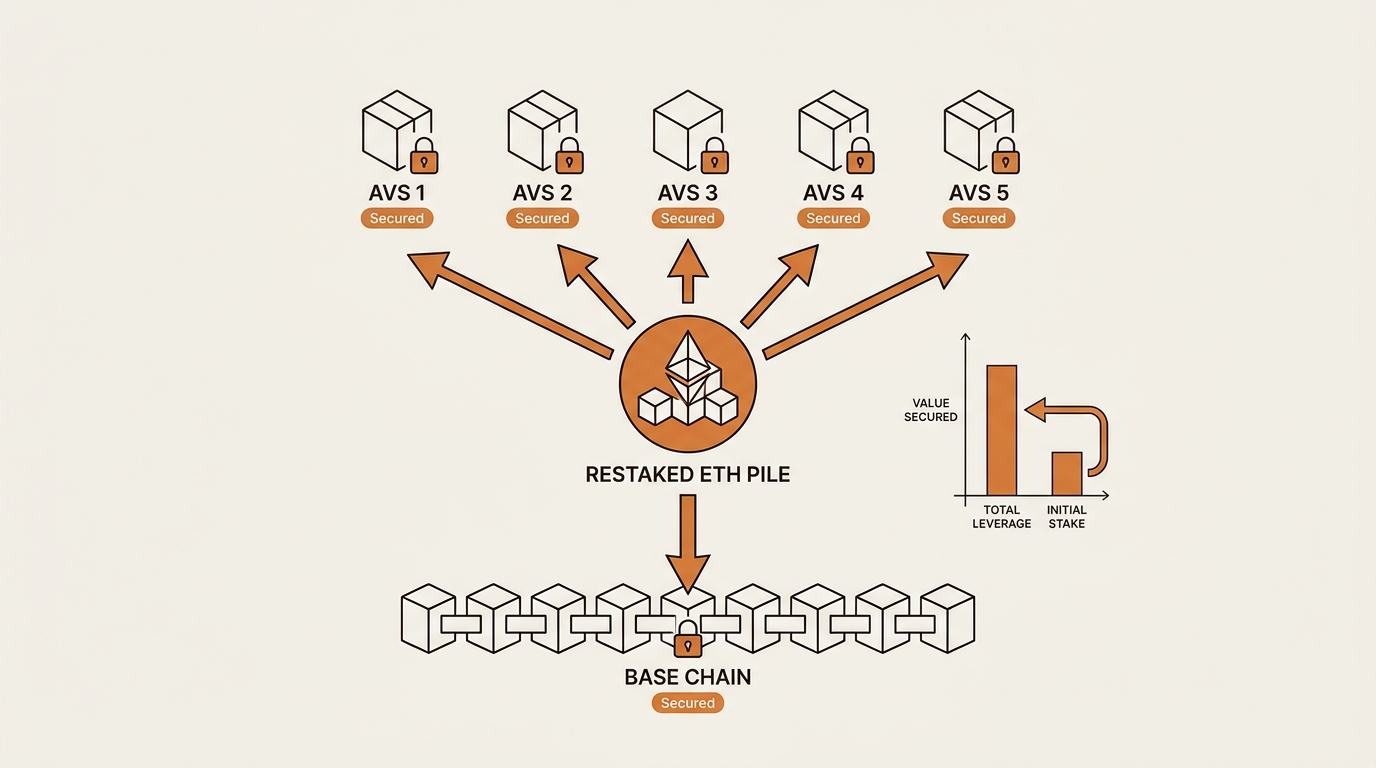

Layer 3 — Restaking. Here is the new idea. Your staked ETH is securing Ethereum, but its economic security is, in a sense, only being used once. Restaking lets that same security be re-pledged to secure other services — oracles, bridges, data-availability layers, and other middleware that need their own crypto-economic backing. On EigenLayer, these services are called AVSs, short for Actively Validated Services. You opt your staked ETH in to back one or more of them, and you earn extra rewards for taking on their slashing conditions too.

Layer 4 — Liquid restaking. Restaking on its own locks you up again. This top floor fixes that the same way liquid staking did one floor down. A protocol restakes for you across a basket of AVSs, manages the operator relationships, and hands you a single LRT — weETH, ezETH, rsETH, and so on — that represents the whole stacked position. You get a tradeable receipt while your ETH quietly works four jobs.

So the full chain is: ETH → staking → LST → restaking → LRT. Five words, and most explainers stop here with a satisfied “and now you earn more.” That is exactly where my first map ended, and exactly where it was broken.

Staking vs liquid staking vs restaking, side by side

Before the part I got wrong, here is the layer map as a table. The question that matters in the last column is not “how much yield” but “what new way to lose did I just sign up for.”

| Layer | What your ETH does | What you hold | New risk you accept |

|---|---|---|---|

| Staking | Secures Ethereum | Locked ETH / validator | Ethereum slashing, illiquidity |

| Liquid staking | Secures Ethereum, but mobile | LST (e.g. stETH) | Protocol smart-contract risk, LST depeg |

| Restaking | Also secures AVSs | Restaked position | AVS slashing on top of base slashing |

| Liquid restaking | Secures AVSs, but mobile | LRT (e.g. weETH) | All of the above, stacked in one token |

Read the last column top to bottom. That is the real product. The yield is the headline; the stacked risk is the body text nobody reads aloud.

Where I drew the map wrong: the rehypothecation layer

This is the part I think about most.

My first mental model was a ladder of separate buckets. Bucket one: ETH secures Ethereum. Bucket two: a fresh, separate stake secures AVS A. Bucket three: another fresh stake secures AVS B. In that picture, more yield came from putting more, separate money to work. Free-ish, because each risk lived in its own bucket.

That picture is wrong, and the word for why is rehypothecation. The same ETH is not split across buckets. It is pledged as security to Ethereum and to several AVSs at the same time. One pile of collateral, backing many promises in parallel. This is the structure EigenLayer is built on, and Consensys spells it out plainly in its breakdown of how restaking and slashing actually work.

Here is the analogy that finally made it click for me, drawn from something every Korean renter understands. A jeonse deposit is the large lump sum you hand a landlord instead of monthly rent. Now imagine you could pledge that one deposit to several landlords at once and collect a little extra from each for the privilege. It feels like income. But if any one of those properties collapses, the claim on your single deposit is triggered — and you only ever had one deposit. The extra yield was never free. It was rent you collected for risk you could not see, because the risk lived in the overlap.

That is what restaking does with slashing. Your staked ETH can be slashed for an Ethereum fault and for the misbehavior of any AVS it backs. The yields add up neatly in a marketing table. The slashing conditions also add up — and they sit on the same collateral. A serious fault at one AVS your operator is securing can take a bite out of the very ETH that is also securing the base chain.

The moment I redrew the map with one shared pile of collateral instead of separate buckets, liquid restaking stopped looking like a free upper floor and started looking like what it is: leverage on risk, paid out as yield.

What liquid restaking tokens actually represent

Once the collateral picture is right, the LRT itself makes more sense. An LRT is a receipt for a managed, restaked position. When you hold weETH or ezETH or rsETH, you are holding a claim on a basket: staked ETH at the base, restaked across some set of AVSs, run through some set of operators the protocol chose.

Three things follow from that, and all three are easy to miss.

First, you are trusting the protocol’s choices, not just Ethereum. Which AVSs it backs, which operators it uses, how it manages slashing exposure — those are decisions made for you, and they shape your risk more than the base layer does.

Second, the LRT is a token with its own market price. It is meant to track the value of the underlying restaked ETH, but in stress it can trade below that value. That is a depeg, and it works on the same mechanics I broke down in how a token holds (or loses) its peg — when everyone wants out at once and the redemption door is narrow, the secondary-market price drops below the “true” backing.

Third, the LRT is composable. You can take it into other DeFi protocols as collateral, borrow against it, farm with it. Each of those adds another layer of smart-contract risk on top of the four already stacked underneath. The convenience is real. So is the pile.

The “8 to 12 percent” number, and why most of it has no price yet

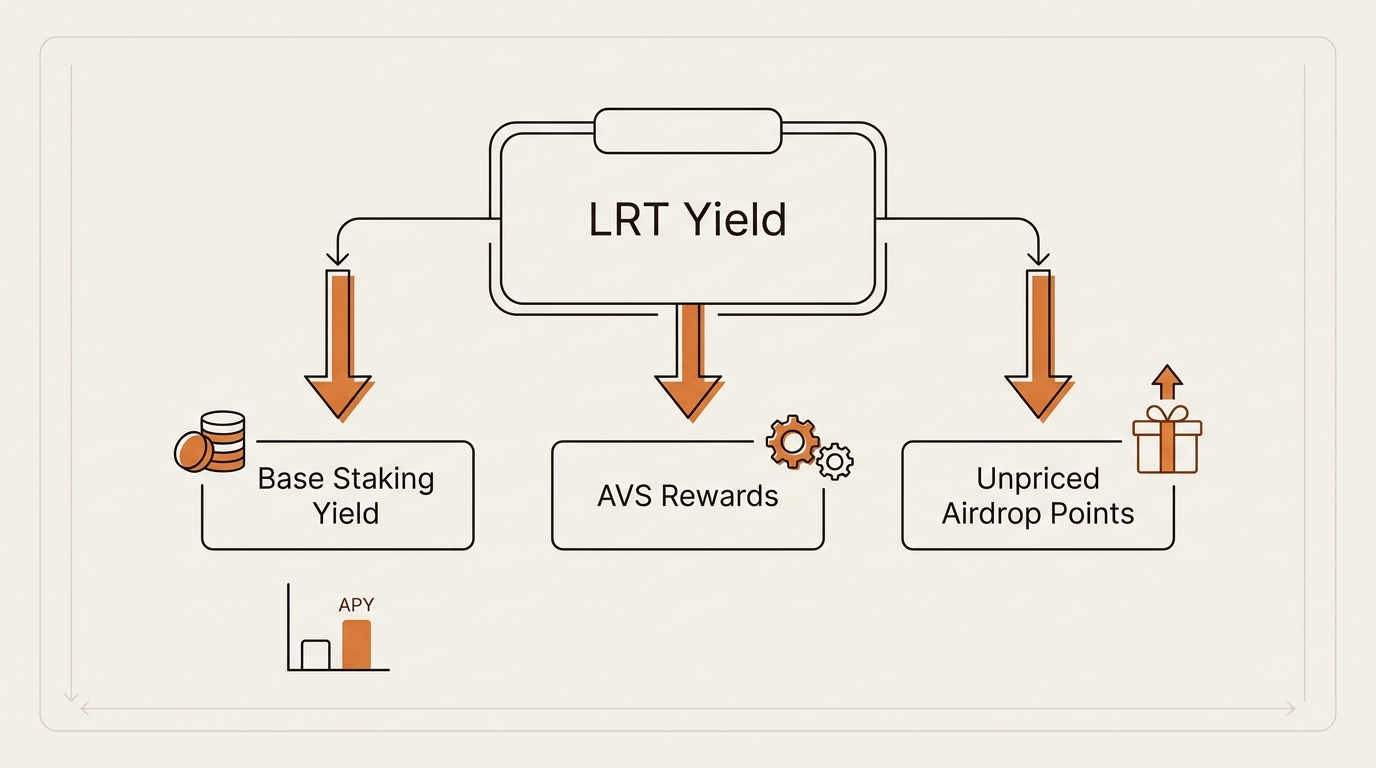

Every LRT pitch leads with a yield figure. I have seen 8 to 12 percent quoted as if it were a savings rate. It is not, and the gap matters.

That displayed number is usually three things added together, only one of which is ETH you can spend today.

The base is real staking yield, paid in ETH, a few percent. On top sit AVS rewards, which are early and variable — some AVSs pay, many barely do yet. And the largest visible chunk is often points: farming credits a protocol issues toward a future airdrop that may or may not happen, at a token price that does not exist yet. Where DeFi yield genuinely comes from is something I unpacked in where DeFi yield actually comes from, and the honest version is that restaking points are not yield in that sense at all. They are a lottery ticket priced as if it had already won.

So the mental separation I now run on any LRT figure: how much of this is ETH in my hand this month, how much is live AVS rewards, and how much is points I am valuing at a number I made up. The displayed APY is a marketing sum of those three. The real economics are mostly in the first one.

The restaking risks nobody puts on the brochure

If the layer map is the structure and rehypothecation is the catch, the risk stack is the part you read before, not after. Here is how I line it up, bottom to top, because a problem at any floor flows upward into your LRT.

Smart-contract risk. Each layer — the LST protocol, EigenLayer, the LRT protocol, any DeFi you take the LRT into — is code that can be exploited. More layers, more contracts, more surface. This is the plainest risk and the one most easily forgotten because it is invisible until it isn’t.

Operator and slashing risk. Your restaked ETH is delegated to operators who run the actual work for AVSs. If an operator misbehaves or an AVS’s slashing conditions are triggered, your collateral is exposed. Because of rehypothecation, that exposure reaches the same ETH securing everything else.

Depeg risk. The LRT can trade below its backing in stress, exactly like a stablecoin under a run. You may hold a token “worth” one ETH that the market will only buy at 0.9.

Exit-queue risk. This is the one the word “liquid” papers over, and it gets its own section.

These are restaking risks that compound rather than sit side by side. A bad event rarely stays on one floor.

The “liquid” in liquid restaking is conditional

The name promises liquidity. The structure delivers it conditionally.

In calm markets, an LRT is liquid in the way the brochure says: there is a deep secondary market, you sell, you are out in seconds. The trouble is that liquidity is exactly the thing that disappears when you most want it.

If you go through the front door — actual redemption back to ETH — you hit a queue. Unstaking from the restaking layer runs through an escrow period measured in days, often around seven to fourteen, and the LRT protocol may add its own withdrawal queue on top. If you go through the side door — selling the LRT on the open market — you are exposed to whatever discount panic buyers demand, which is the depeg again. In a real stress event, both doors narrow at the same time. The escrow makes the front door slow, the depeg makes the side door expensive, and “liquid” turns out to mean “liquid until everyone needs it to be.”

This is the same gap between a comforting name and the structural reality that shows up across crypto, and learning to read the structure instead of the label is the whole habit I am after — the same one behind reading crypto structure instead of price. The word “liquid” is a feature in good weather and a marketing claim in bad weather. Plan for the bad weather, because that is when you find out which one it was.

How I actually read an LRT now, in order

This is the sticky-note version — the order I run before deciding whether I even understand a restaked position, never mind hold one.

- Draw the layers. ETH → LST → restaking → LRT. If I cannot name what is at each floor, I do not understand the thing yet.

- Find the shared collateral. Remember it is one pile backing many promises, not separate buckets. Ask which AVSs and operators that pile is exposed to.

- Split the yield. Base ETH yield, live AVS rewards, and unpriced points are three different things wearing one number.

- Map the exits. How long is the escrow, is there a protocol queue, and how deep is the secondary market on a bad day.

- Count the contracts. Every layer is code. The LRT in another DeFi protocol is one more.

No prediction about which LRT wins. No ticker to go buy. Just the map, redrawn with the layer I missed the first time put back in.

FAQ

How do liquid restaking and LRTs work in one sentence? Liquid restaking takes ETH that is already staked, re-pledges its security to additional services called AVSs, and gives you a tradeable token — an LRT — that represents the whole stacked position. You keep something liquid while your ETH earns from doing more than one job at once.

What is the difference between staking, liquid staking, and restaking? Staking locks ETH to secure Ethereum and earns a base reward. Liquid staking does the same but gives you a tradeable LST so your stake stays mobile. Restaking re-pledges that already-staked ETH to secure extra services for extra reward — and extra slashing exposure. Liquid restaking adds a tradeable token on top of restaking.

What is the difference between an LRT and an LST? An LST, like stETH, represents ETH staked once, securing only Ethereum. An LRT, like weETH, represents ETH that is staked and then restaked across additional AVSs. The LRT carries everything the LST does plus AVS slashing and operator risk, stacked on the same collateral. More layers, more yield, more ways to lose.

Can I lose my ETH through slashing in restaking? Yes, in principle. Slashing can remove part of your staked ETH for an Ethereum-level fault and, because of restaking, for the misbehavior of AVSs your collateral backs. Since the same ETH secures several things at once, a serious fault at one layer can reach the shared collateral underneath your whole position.

Is the displayed liquid restaking APY real yield? Partly. The figure usually combines real ETH staking yield, early and variable AVS rewards, and points toward a possible future airdrop. Only the first is ETH you can spend today. The points are valued at a token price that does not exist yet, so a headline like “10 percent” is a marketing sum, not a savings rate.

How long does it take to withdraw from an LRT? It depends on the door you use. Redeeming back to ETH runs through a restaking escrow of roughly seven to fourteen days, plus any queue the LRT protocol adds. Selling the LRT on the open market is faster but exposes you to a depeg discount in stress, when both the queue and the market tighten at the same time.

Next in this series

The map above shows the layers and the risk stack. The next post in Crypto Mental Models takes a single LRT depeg event and walks the failure upward floor by floor — which layer cracked first, how the escrow and the secondary market reacted, and what the order of events teaches about reading any stacked-collateral product. Same map, traced backward from a break.

For now, the reframe I would leave on the sticky note: liquid restaking is not a second yield on the same ETH. It is rent you collect for risk you can’t see — so map the risk stack before you ever read the APY.

seonjae — Korean office worker documenting his transition into AI systems, agents, and vibe coding — without a CS background. Shipping in public.