What Is a Stablecoin and How Does It Work? My Framework

What Is a Stablecoin and How Does It Work? A Non-Developer’s Three-Question Framework

Most articles answering what is a stablecoin and how does it work stop at the definition. This one starts there and keeps going.

If you have been searching what is a stablecoin and how does it work, you have already noticed that every result tells you the same five sentences. A token pegged to a dollar. Backed by reserves. Used on-chain. That part is true, and useless. The useful part is what you do with that knowledge.

I am not a trader. I am a Korean office worker who reads on-chain data on weeknights with a coffee, and I have spent more time studying the March 2023 USDC weekend than I have spent holding any single stablecoin. That is on purpose. The thing I needed was not a list of tokens. It was a mental model I could run on any stablecoin in under sixty seconds, before deciding whether the thing on my screen behaves like cash, like a money market fund, or like neither.

Here is what you get in this piece: the shortest honest definition, then a three-question frame I now use, then the 2023 USDC depeg as a teaching case, and finally a side-by-side of a bank dollar versus a USDC dollar that I wish someone had put in front of me two years ago.

The shortest honest definition

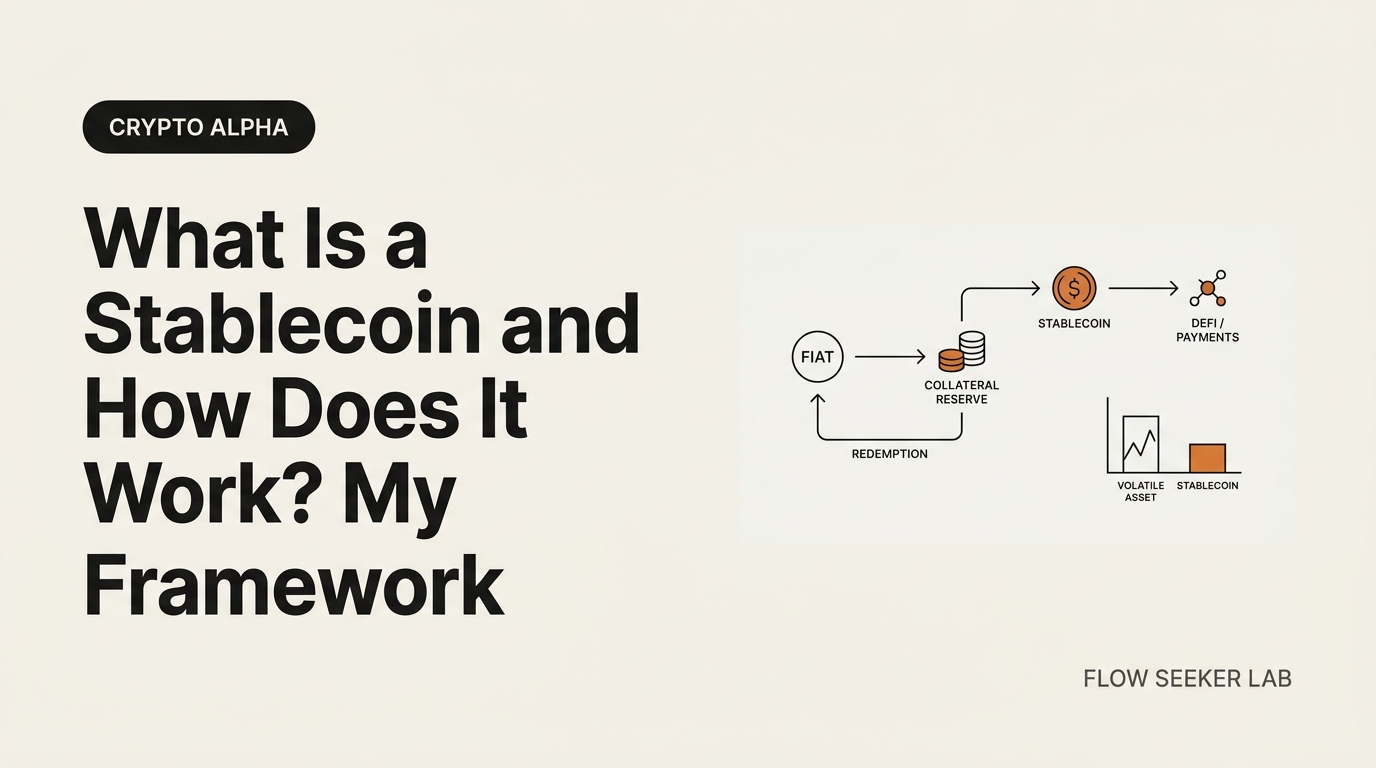

A stablecoin is a cryptocurrency token engineered to hold a stable price against a reference asset, almost always one US dollar, by holding reserves or running a mechanical peg. Some are backed one-to-one by cash and short-dated Treasuries at a regulated issuer. Some are backed by other crypto, locked at more than one hundred percent collateral inside smart contracts. Some used to be backed by nothing but an algorithm, and those have mostly failed.

That is the textbook part. The Bank of England has a clean version of the same definition if you want a central bank framing of what stablecoins are and how they work. The interesting part starts when you ask why the price actually stays at one dollar, and what happens when it does not.

Why a non-developer should even care

In Korea there is essentially no KRW stablecoin in retail use. So for a Korean office worker the whole category feels abstract at first — dollars on a chain, fine, but I get paid in won and I pay rent in won. That was my reaction for a long time too.

What changed my reading was noticing how often the dollar leg of crypto already touches my life without asking. Friends who freelance for US clients get paid in USDC because the wire takes three days and the stablecoin takes thirty seconds. A founder I know parks a runway in stablecoins because his banking partner is shaky. None of them are trading. They are using a stablecoin as a wire that does not sleep on weekends.

That is the question worth holding in your head while reading the rest. Not should I buy a stablecoin. The question is: what kind of dollar is this, exactly, and what backs it.

The three-question frame

This is the actual framework. When someone hands you a stablecoin ticker — USDC, USDT, DAI, FRAX, PYUSD, whatever new one launched last month — you run three questions in this order. Each question rules out a category of failure.

Q1. Who holds the reserve, and what is it?

A stablecoin promising a dollar is only as good as the assets sitting behind it. Cash in a regulated bank is one thing. Short-dated US Treasuries at a custodian is another. Commercial paper from a Chinese property developer is a very different thing. An on-chain pool of volatile crypto, locked at 150% collateral, is a fourth category entirely. Nothing at all — pure algorithmic balance — is the fifth, and that one has a graveyard.

So before anything else: name the assets, name the custodian, and check whether the issuer publishes attestations from a real auditor.

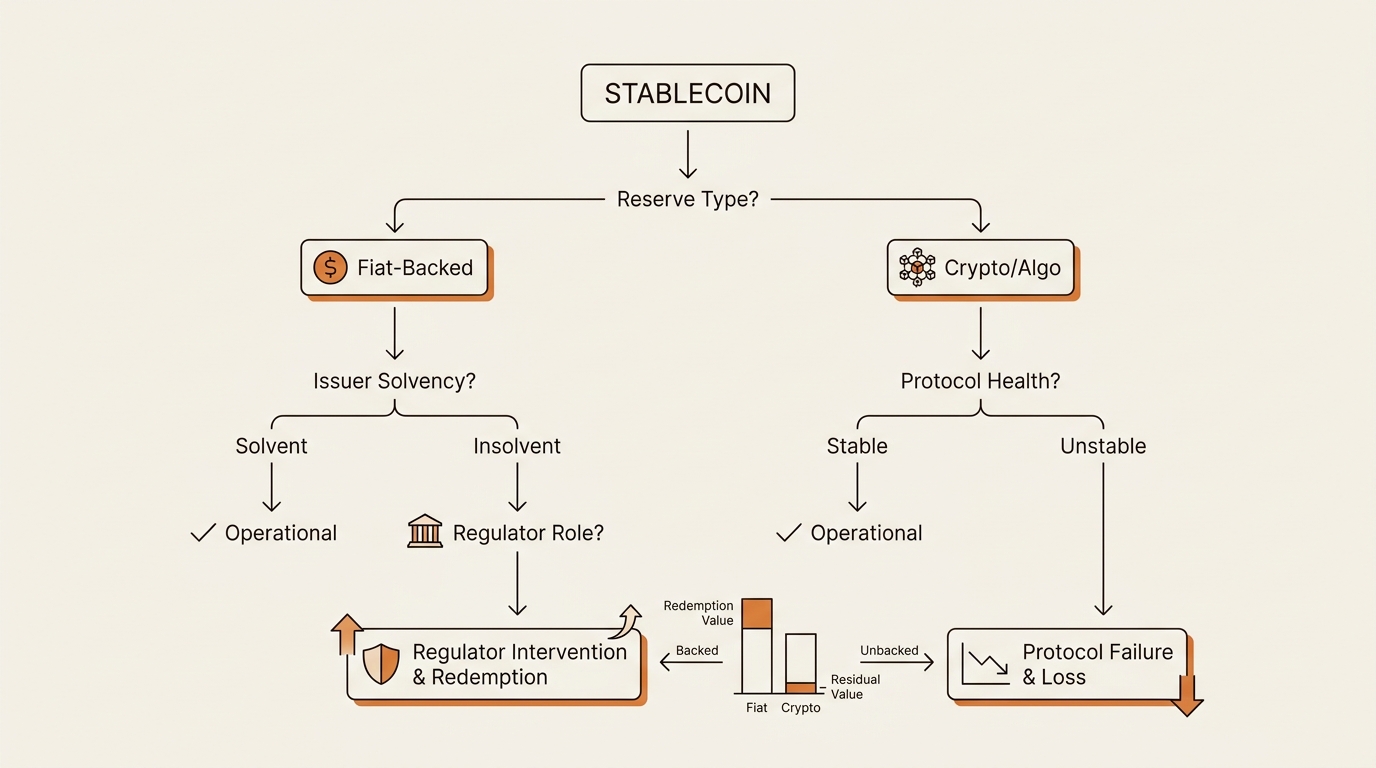

Q2. What happens if the issuer disappears tomorrow?

This is the question almost no marketing page answers. Pretend the company behind the token files for bankruptcy this weekend. What do you actually own?

For Circle’s USDC, you own a claim on segregated reserves held in regulated US institutions, mostly short-dated Treasuries. For Tether’s USDT, you own a claim on Tether Limited’s balance sheet — historically more opaque, now partly disclosed quarterly. For MakerDAO’s DAI, you own a claim that is enforced by a smart contract that auctions the collateral if the system gets unhealthy; the “issuer” is not a single legal entity. For an algorithmic stablecoin with no reserve, you own a promise that depends on the system staying liquid — and when it does not, you own nothing, which is the lesson the TerraUSD collapse taught at a cost of around $40 billion in market value.

Q3. Who regulates it, and what does that regulation actually require?

The regulator is not just a logo. It defines what the issuer must hold, where they must hold it, and how often you can redeem it. Under the EU’s MiCA framework, fiat-backed e-money tokens must be one-to-one backed with reserves in EU bank custody. Under the US GENIUS Act passed in 2025, licensed payment stablecoin issuers must hold reserves in cash or short-dated Treasuries and — this is the important one for retail users — cannot legally pay interest on the stablecoin. Offshore unregulated issuers are bound by whatever their home jurisdiction enforces, which is sometimes very little.

That third question is the one I run last because it is the one that changes most. Reserves move slowly. Issuer structures move slowly. Regulation can move in a single quarter and rewrite what a stablecoin even is.

Here is how the three questions map to the four major designs side by side.

| Stablecoin | Q1 Reserve | Q2 If issuer disappears | Q3 Regulation |

|---|---|---|---|

| USDC (Circle) | Cash + short Treasuries at regulated US custodians | Claim on segregated reserve | US state money transmitter + GENIUS Act path |

| USDT (Tether) | Mix of Treasuries, secured loans, gold, bitcoin | Claim on Tether Ltd balance sheet | Mostly offshore (BVI); no US license |

| DAI (Maker) | On-chain ETH, USDC, real-world assets at roughly 150% collateral ratio | Smart contract auctions the collateral | Decentralized protocol; not a licensed issuer |

| TerraUSD (UST, defunct) | Algorithmic mint/burn with LUNA, no reserve | Nothing | Unregulated |

Notice the column that does the work is Q2. The first column tells you what they say is there. The second tells you what you actually own in the bad case.

Holding dollars in a bank versus holding USDC

The cleanest way to feel the trade-off is to put a US bank deposit and a USDC balance next to each other and ask how each one behaves on the dimensions that matter to a normal user. This is not a recommendation. It is a framework for understanding what you are actually choosing between.

| Dimension | $1,000 in a US bank | $1,000 in USDC in a wallet |

|---|---|---|

| Insurance | FDIC up to $250,000 per depositor | None — claim on issuer’s reserve |

| Yield | Savings account interest (regulated, taxed) | Zero by law in the US under the GENIUS Act |

| Settlement speed | 1–3 business days for ACH | Seconds on-chain |

| Operating hours | Bank business hours, weekday cutoffs | 24/7, including weekends |

| Counterparty risk | The bank — backstopped by FDIC and Fed | The issuer + the bank holding the cash leg |

| Reversibility | Some chargeback / dispute paths | None — on-chain transfers are final |

| Cross-border friction | High; wires, correspondents, days | Low; one chain, one transfer |

The honest reading is that USDC is not safer than a bank deposit. It is not less safe either. It trades a regulated insurance backstop for cross-border speed and weekend availability, and it does so for users whose biggest problem is getting a dollar from A to B rather than protecting a dollar that already sits at A. That is a real use case. It is just a different one.

For a deeper view on the dollar-versus-stablecoin question, the Federal Reserve has published a primary-source analysis of the SVB failure and its impact on stablecoins that I keep going back to.

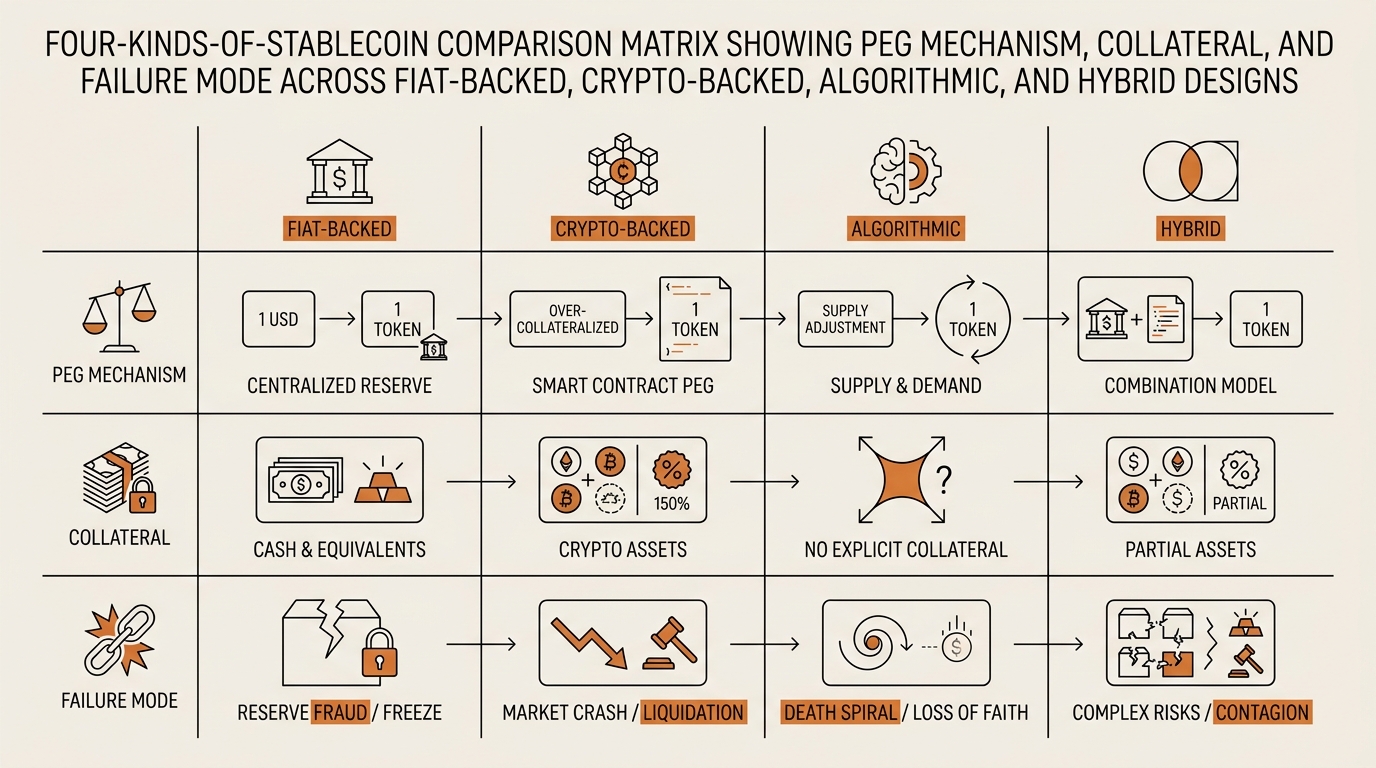

The four kinds of stablecoin, and what each one trades off

The three questions above are mechanical. The four kinds below are the categories the questions fall into. You need both, because the question runs the same on every token, but the answer pattern is category-specific.

Fiat-collateralized. USDC, USDT, PYUSD, FDUSD. The simplest mental model: a company holds dollars and Treasuries, issues tokens against them, and promises one-to-one redemption. Trade-off: cleanest peg, simplest story, but you absorb full counterparty risk on the issuer and on the bank holding the cash. The Silicon Valley Bank weekend in March 2023 was the textbook lesson here, and we will get to it.

Crypto-collateralized (over-collateralized). DAI, LUSD, GHO. The mental model is a smart contract pawnshop. You lock $150 of ETH and the contract lets you mint $100 of stablecoin. If the collateral falls in price, the contract auctions it before the peg breaks. Trade-off: no traditional bank counterparty risk, but exposure to crypto-collateral volatility and oracle risk. The over-collateralization model is the same one I broke down in how Aave interest rates work — same logic, different product.

Algorithmic. Mostly historical. TerraUSD/UST is the canonical case: no reserve, only a mint-and-burn relationship with a volatile sister token (LUNA). When confidence cracked in May 2022, the design unwound in days. Trade-off: extreme capital efficiency in calm markets, total failure mode in stress. The category is not dead in research, but no algorithmic stablecoin has reached durable scale post-Terra.

Hybrid. FRAX (until its v3 redesign), USDD, and several newer designs blending fiat collateral with on-chain mechanisms. Trade-off: complexity. You are not running one mental model — you are running two stacked, and the failure modes can interact in ways that are hard to predict until they happen.

What broke: the March 2023 USDC weekend, and what my mental model got wrong

This is the part I think about more than any other.

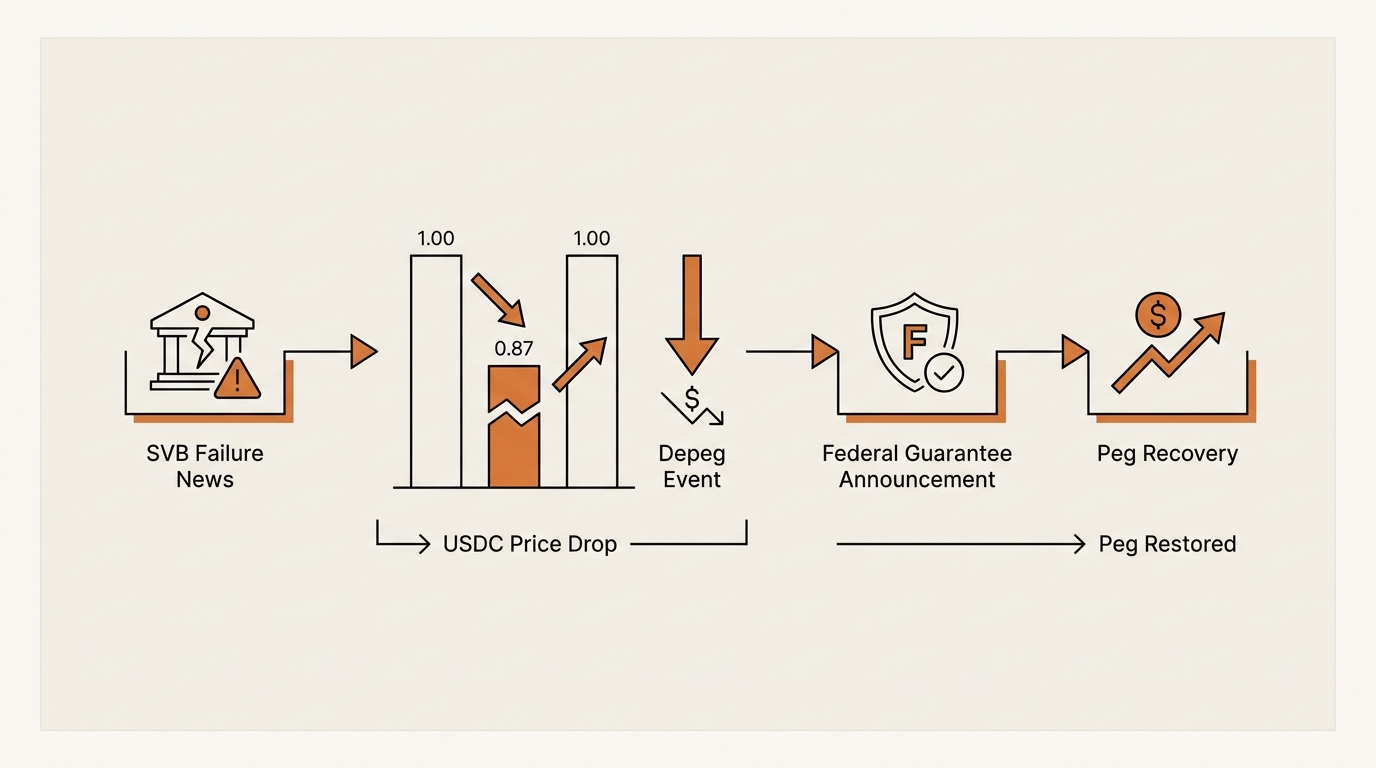

On Friday March 10, 2023, Silicon Valley Bank collapsed. Circle, the issuer of USDC, disclosed late that night that around $3.3 billion of its cash reserves — roughly 8% of total USDC backing — was held at SVB. Over the weekend the USDC price on secondary markets fell from about $1.00 to around $0.87, as CNBC reported at the time. On Sunday March 12, US regulators announced they would guarantee SVB depositors in full. By Monday morning USDC was back at one dollar.

The peg held. The mechanism worked. But the lesson I took away the next morning was not “USDC is safe, the system worked.” It was that my mental model of “one-to-one backed equals safe like a bank” had been quietly wrong for two years.

Here is what I had assumed: a fully reserved stablecoin is a digital warehouse receipt. Cash goes in, token comes out, and as long as the cash is really there, the token is really a dollar.

Here is what was actually true: a fully reserved stablecoin is a claim on a portfolio held at a set of banks and custodians. That portfolio is only as safe as its weakest leg. If the bank holding any meaningful portion of the cash leg fails on a Friday afternoon, the market reprices the token before the regulator opens on Monday. The peg did not break because the reserve was wrong. It broke because the bank holding part of the reserve was wrong, and the market had to live with that uncertainty for forty-eight hours.

That is a transferable mental model. It applies to money market funds. It applies to corporate deposits. It applies, in a sideways way, to my own checking account, which is also a claim on a bank that holds my cash among other claims.

What I do differently now: when I look at any fiat-backed stablecoin, I do not stop at “is it backed.” I ask “where is the cash leg, and what would a bad weekend at that bank look like.” That is what the BIS working paper on public information and stablecoin runs digs into formally, and it is what the Brookings stablecoin regulation explainer gestures at from a policy angle. The reserve is a portfolio. Portfolios have weakest links.

Regulation, briefly: MiCA, the GENIUS Act, and why “no yield” matters

I am not going to predict where regulation is heading. But the current shape of it changes the answer to Q3 enough that you should know the broad strokes.

In the EU, the Markets in Crypto-Assets regulation — MiCA — went fully into effect in mid-2024 for stablecoin issuers. The short version: fiat-referenced e-money tokens must be one-to-one backed, with reserves held in segregated accounts at EU-authorized institutions, and issuers must be licensed as electronic money institutions or credit institutions.

In the US, the GENIUS Act passed in 2025 created the first federal payment stablecoin license. Licensed issuers must hold reserves in cash or short-dated Treasuries at qualifying institutions, publish monthly disclosures, and — the line that catches almost everyone off guard — they cannot pay interest on the stablecoin to holders. That is by design. The regulator wanted a payment instrument, not a deposit substitute that competes with insured bank accounts.

What this means for the three-question frame: Q3 now has actual answers in two of the world’s largest jurisdictions. A stablecoin without a path to either license is, in 2026, increasingly a different product than one with that license. Not better or worse, in the abstract. But the failure modes are different, and the framework has to account for it.

How I actually run the three-question frame before holding any stablecoin

This is the checklist version. It is what I would write on a sticky note if a friend asked.

- Open the issuer’s reserves page. Name the top three asset categories. If you cannot find a reserves page in two minutes, that is itself the answer.

- Find the most recent attestation. Check who signed it. A Big Four name and a date within the last quarter is one signal. No attestation, or an attestation older than six months, is another.

- Identify the bank or custodian holding the cash leg. Ask the SVB question: what would a bad weekend at that bank look like?

- Check the regulatory status. MiCA-licensed? GENIUS Act-licensed? Offshore? None of the above? Each answer changes what you are actually holding.

- Look at on-chain depth. Is there enough liquidity on major venues to redeem at scale, or only at retail size? This is where reading on-chain data earns its keep — the reserve PDF tells you what the issuer claims, the chain tells you what the market thinks.

- If you cannot answer Q1, Q2, and Q3 in under five minutes, the framework’s verdict is to wait. Stablecoins should be a base, not a bet — the same logic as bases before bets.

That is the whole frame. No prediction about which stablecoin “wins.” No exchange recommendation. Just the questions in the order I learned to ask them, after watching the March 2023 weekend with no skin in the game and realizing my model of money had been quietly wrong.

FAQ

Are stablecoins actually safe to hold? Safety is the wrong word for the question. Stablecoins are not safer or less safe than a bank deposit in the abstract — they are differently safe. A regulated fiat-backed stablecoin removes the bank’s interest payment and the FDIC backstop, and adds 24/7 settlement and counterparty exposure to the issuer’s reserves. Run the three-question frame on the specific token and you will know what you are exposed to.

USDT versus USDC — what is the actual difference? Both are fiat-collateralized stablecoins pegged to the US dollar. USDC is issued by Circle, regulated in the US, and holds reserves primarily in cash and short Treasuries at regulated custodians with monthly attestations. USDT is issued by Tether, headquartered offshore, holds a more diverse reserve mix including secured loans and bitcoin, and publishes quarterly attestations. The peg behaves similarly day to day. The Q2 answer — what you own if the issuer disappears — is structurally different.

How do stablecoin issuers make money? On the float. An issuer holds billions of dollars of customer reserves in short-dated US Treasuries that currently yield around 4 to 5 percent annually, and they keep that yield. Under the GENIUS Act, regulated US payment stablecoin issuers cannot pay that yield to holders, which means the issuer’s net interest margin is the whole business model. This is why stablecoin economics scale linearly with circulating supply.

What happens when a stablecoin loses its peg? The short answer depends on the kind. A fiat-backed stablecoin can trade below peg if the market doubts the reserve, as USDC did briefly in March 2023, and recover once the reserve is confirmed solvent. A crypto-backed stablecoin can break if the underlying collateral falls faster than the contract can auction it. An algorithmic stablecoin can spiral irreversibly, which is what happened to TerraUSD in 2022.

Is a stablecoin the same as holding dollars in a bank? No. A US bank deposit is FDIC-insured up to $250,000, pays regulated interest, and settles through traditional rails on bank business hours. A US-regulated stablecoin is a claim on the issuer’s reserve portfolio, pays no interest by law, and settles on-chain 24/7 in seconds. They solve different problems for different users. Treating them as identical is the most common beginner mistake.

Do US and EU regulations treat stablecoins the same way? Broadly similar in spirit, different in detail. Both require one-to-one fiat reserves, both require licensed issuers, both require disclosures. The EU’s MiCA is fully in force across all member states. The US GENIUS Act creates a federal path that runs in parallel to existing state money transmitter regimes. The biggest practical difference for retail users: where the reserve is custodied, and which regulator you appeal to if something goes wrong.

Next in this series

The framework above tells you what to look for. The next post shows the receipts — how to verify a stablecoin’s reserves on-chain yourself, without trusting the issuer’s PDF, using free tools any non-developer can run from a browser. Same three questions, different lens.

Together they are the long answer to what is a stablecoin and how does it work — not the textbook definition, but the working model I run before I ever click swap.

seonjae — Korean office worker documenting his transition into AI systems, agents, and vibe coding — without a CS background. Shipping in public.